5 Ways to Find Grid Connection Capacity in Saturated Iberia

April 7, 2026

The Iberian Peninsula has a problem that sounds paradoxical: it has built one of Europe's most impressive renewable fleets, and now it is running out of places to plug new projects into the grid.

In Spain, 88% of distribution nodes are saturated, and only 12% of grid access requests were approved in 2025.

For developers and investors, that changes the playbook. The old approach, find the sunniest site first and figure out the grid later, no longer works.

But this is not an impossible market. It is a puzzle, and puzzles reward the teams that can see the full picture.

Capacity will appear across the Iberian grid over the next five years at specific nodes and in specific windows, driven by infrastructure investments, expiring permits, and shifting demand patterns. The real question is whether you can see those openings forming before everyone else does.

Here is a five-point framework for investors who want to turn the grid problem into an opportunity.

1. Start from the grid, not the resource

This is the biggest mental shift in renewable investing today, and one of the most valuable.

For two decades, developers started with the resource: the best irradiance, the strongest winds, or the lowest-cost land. The grid came later.

In today's Iberia, that logic has flipped. Spain does not lack solar resource. It lacks the grid capacity to deliver it. Portugal's best wind corridors face the same problem.

If you start from resource quality alone, you are often led straight to the most crowded nodes on the map, the ones where curtailment is already severe and zero-price hours are becoming more frequent.

Instead, start from the grid.

Identify the nodes that can realistically host your project across the three technical criteria that determine access:

- Short-circuit strength

- Static limits

- Dynamic stability

Then check the resource. In many cases, a site with slightly lower irradiance but a clear grid path produces far better economics than a prime solar location where a large share of output never reaches the market.

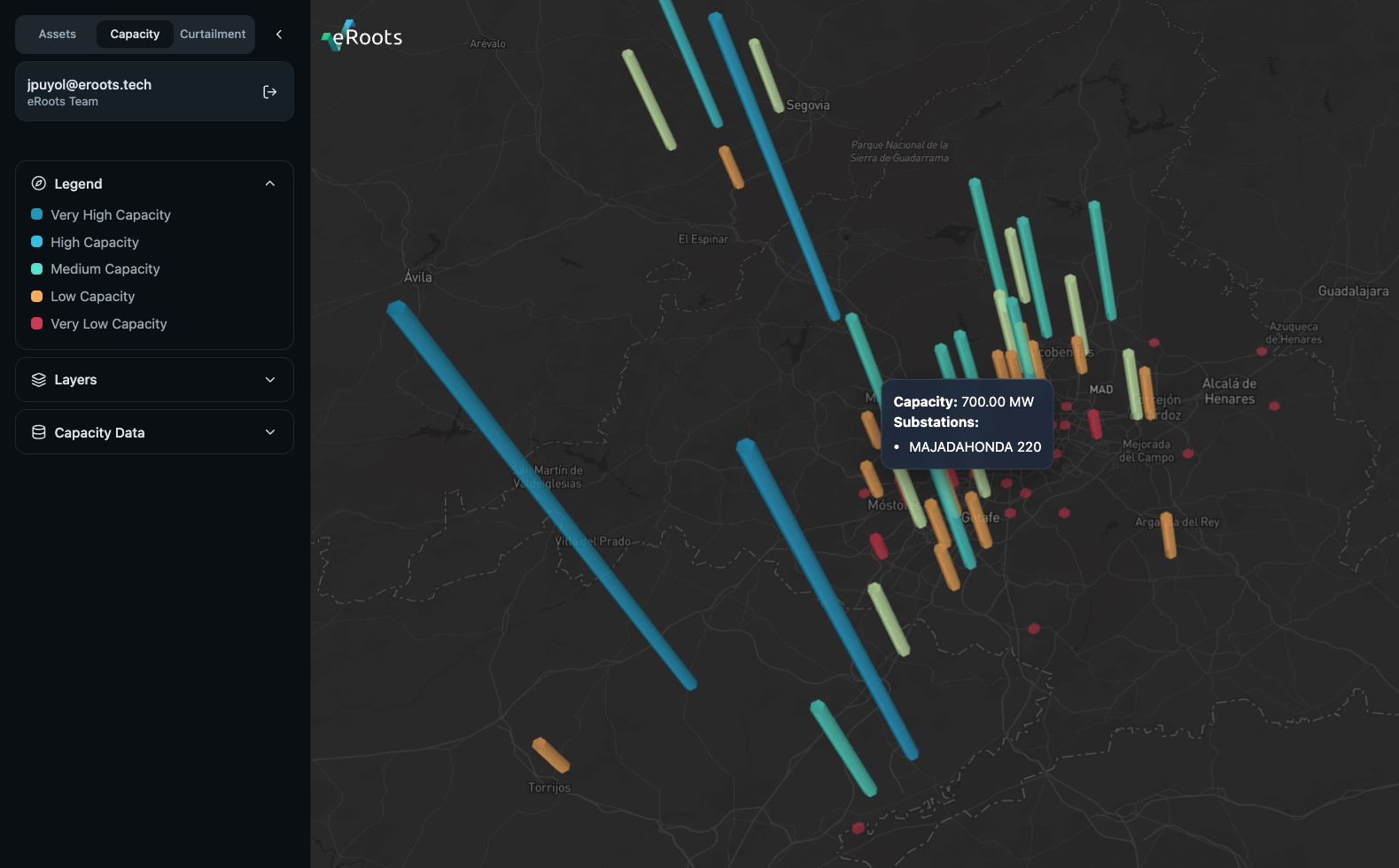

This is exactly what eRoots Map was built for. Instead of screening hundreds of sites and discovering that almost none have viable access, teams can begin with the nodes where connection is technically feasible and build their strategy outward.

2. Look at where capacity is going, not just where it is

Public capacity maps from REE and the distribution companies are only a snapshot of today.

They tell you what is full right now. They do not tell you what may open next year, or in 2029 when a new 400 kV corridor enters service.

The investors who get ahead are the ones who can read the grid forward in two directions.

Where capacity is being built

REE's 2026-2030 plan proposes 422 connection expansions and 27.7 GW of new demand access capacity, a major increase over the current cycle.

That capacity will not arrive everywhere at once. It will land at specific substations, in specific corridors, and on specific timelines. If you can map which reinforcements unlock which nodes and when, you can secure land and strategic positions before the capacity shows up on any public map.

Where capacity is about to free up

Spain has 129 GW of granted generation permits on the transmission grid, many of them held by projects that may never be built.

The regulatory milestone regime steadily removes stale permits. Tracking which permits are approaching their deadlines, and at which nodes, helps reveal where so-called phantom capacity may soon return to the system.

Both of these dynamics require simulation, not just map reading. eRoots integrates the REE investment timeline and the permit pipeline into scenario analysis so teams can explore future capacity openings interactively instead of piecing together spreadsheets after the fact.

3. Understand why a node is constrained, and design around it

Not all grid constraints are the same.

At each node, available capacity is limited by whichever technical criterion becomes restrictive first, and each type of constraint has a different solution, cost profile, and timeline.

If the constraint is grid strength

The node may lack enough synchronism to stabilize inverter-based renewables. In some cases, adding assets such as synchronous condensers can unlock capacity that otherwise appears unavailable.

If the constraint is thermal

Lines or transformers may already be near their limits. This often requires TSO reinforcement, but smart project sizing or future dynamic line rating can sometimes create a workable path without waiting for a full network upgrade.

If the constraint is dynamic stability

This is becoming more common, especially under tighter post-blackout security requirements. It is also where storage can be especially powerful. Batteries with fast frequency response do not just fit into constrained nodes; they can actively improve local stability and create new headroom.

The practical takeaway is simple: a node labeled "no capacity available" on a static map may still have a viable route for the team that understands what is actually binding.

4. Think in pairs: generation meets demand

The grid is a two-sided system. What matters is not only how much power you inject, but also the balance between generation and consumption at each node.

Spain's 2026-2030 planning explicitly prioritizes new demand connections such as data centers, green hydrogen, and industrial electrification.

That means some nodes that are currently saturated for generation could become viable if a large consumer connects nearby. New demand absorbs local generation, reduces curtailment, and improves the node's price profile.

This creates room for more creative strategies.

A solar plant co-located with a data center or electrolyzer is not just a compelling commercial story. It can also be a grid-feasibility strategy. The combined project may pass access criteria that neither project would satisfy alone, because the net flow into the wider grid is much lower.

For storage investors, the same logic works in reverse. The nodes where generation developers are struggling most are often the nodes where batteries can capture the most value. Storage can reshape the local load profile, absorb cheap midday energy, and improve conditions for future connections.

5. Treat financial guarantees as strategic bets

At EUR40 per kW, Spain's financial guarantee system turns every grid access application into a meaningful capital allocation decision.

A 200 MW portfolio can lock EUR8 million for years. In a constrained and fast-moving grid, that is not just an administrative requirement. It is a strategic bet on whether the chosen node will still look attractive by the time the project is ready to operate.

The risk is not only losing the guarantee if milestones are missed. It is also committing capital to a node that looked attractive at filing time but deteriorates as more projects cluster there, curtailment rises, and capture prices fall.

Disciplined investors treat each guarantee as an option backed by a forward view:

- What does this node look like in 2028-2030 under different generation and demand scenarios?

- What is the likely curtailment trajectory?

- Which grid reinforcements are committed, and which are still uncertain?

If the outlook weakens, it may be smarter to exit early and reallocate capital to a stronger node than to chase a weak project all the way to commissioning.

The bigger picture

The Iberian grid constraint is real and structural, but it is not a wall. It is a puzzle.

Over the next five years, grid investment will reshape where capacity exists. Stale permits will expire. New demand from electrification and digitalization will rebalance flows in ways that create openings most market participants are not tracking yet.

The teams that thrive will not be the ones with the largest pipelines on paper. They will be the teams that understand where their megawatts actually fit in the grid, and who get there first.

The era of resource-first planning is behind us. What comes next is grid-intelligent planning.

If you are allocating capital in Iberia and want a clearer view of where real opportunities are forming, contact the eRoots team or explore eRoots Map to evaluate current and future connection capacity across the Iberian grid.